What You Can and You Can’t Claim – Vehicle and Travel Expenses

VEHICLE AND TRAVEL EXPENSES

The ATO allows you to claim vehicle and travel expenses only in certain cases, even your normal trips between home and work. Check here all the cases you can claim vehicle and travel expenses and if you are eligible or not.

The first thing to have in mind is to keep a record of all your travel expenses, including car, fuel and parking. Learn here how to calculate your car expenses.

TRAVELS BETWEEN HOME AND WORK

Trips between home and work are generally considered private travel. In some circumstances, you can claim a deduction for travel between home and work, as well as for some travel between two workplaces.

If your travel was partly private, you can only claim what you incurred in the course of performing your work duties.

You can claim the cost of travelling:

✅ Directly between two separate workplaces – for example, when you have a second job (if one of these places isn’t your home).

✅ From your normal workplace to an alternative workplace that is not a regular workplace (for example, a client’s premises) while still on duty, and back to your normal workplace or directly home.

✅ If your home was a base of employment – you’re required to start your work at home then travel to a workplace to continue your work for the same employer.

✅ If you had shifting places of employment – you regularly work at more than one site each day before returning home.

✅ From your home to an alternative workplace that is not a regular workplace for work purposes, and then to your normal workplace or directly home. This doesn’t apply where the alternative workplace has become a regular workplace.

✅ If you need to carry bulky tools or equipment that your employer requires you to use for work which you can’t leave at your workplace – for example, an extension ladder or a cello.

You can’t claim the cost of driving your car between work and home just because:

❌ You do minor work-related tasks – for example, picking up the mail on the way to work or home.

❌ You have to drive between your home and your workplace more than once a day.

❌ You are on call – for example, you are on stand-by duty and your employer contacts you at home to come into work.

❌ There is no public transport near where you work.

❌ You work outside normal business hours – for example, shift work or overtime.

❌ Your home was a place where you ran your own business and you travelled directly to a place of work where you worked for somebody else.

❌ You do some work at home.

VEHICLE EXPENSES

If you use your own vehicle in performing your work-related duties (including a car you lease or hire), you may be able to claim a deduction for car expenses.

If the travel was partly private, you can claim only the work-related portion.

This information relates to car expenses only. A car is defined as a motor vehicle (excluding motor cycles and similar vehicles) designed to carry a load less than one tonne and fewer than nine passengers. Many four-wheel drive vehicles are included in this definition.

If you use someone else’s car for work purposes, you may be able to claim the direct costs (such as fuel) as a travel expense (see Other travel expenses).

For other vehicles (that are not cars), see Other travel expenses. Other vehicles include:

Motorcycles

Vehicles with a carrying capacity of:

One tonne or more (such as a utility truck or panel van)

Nine passengers or more (such as a minivan).

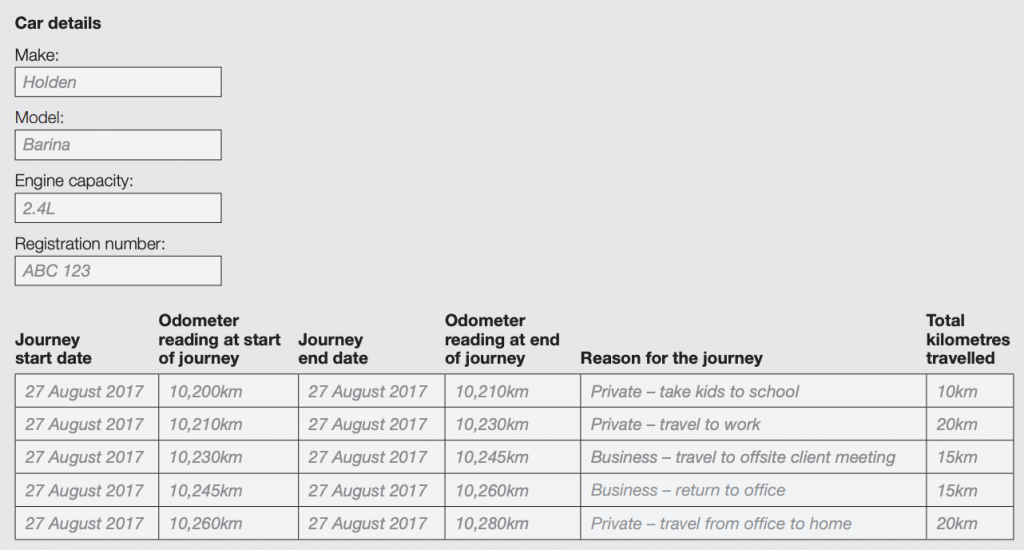

When working out your claim, you need to use the actual costs of your motor vehicle expenses. You need to keep receipts for the actual costs you incur such as petrol and oil. You can use a logbook or diary to separate private use from work-related trips.

You can claim a deduction for work-related car expenses if you use your own car in the course of performing your job as an employee – for example, to:

✅ Carry bulky tools or equipment (such as an extension ladder or cello) that your employer requires you to use for work and there is no secure storage available at work.

✅ Attend work-related conferences or meetings away from your normal workplace.

✅ Deliver items or collect supplies.

✅ Travel between two separate places of employment, but not if one of the places is your home (for example, when you have a second job).

✅ Travel from your normal workplace to an alternative workplace (that isn’t a regular workplace) back to your normal workplace or directly home.

✅ Travel from your normal workplace or your home to an alternative workplace that is not a regular workplace – for example, a client’s premises

✅ Perform itinerant work.

If you receive an allowance from your employer for car expenses, it is assessable income and the allowance must be included on your tax return. The amount of the allowance is usually shown on your payment summary or income statement.

You can’t claim a deduction for car expenses that have been salary sacrificed or where you have been reimbursed for these expenses.

❌ For motorcycles and other vehicles (that are not cars), you can’t claim work-related deductions under car expenses. However, you may be able to claim for work-related deductions under travel expenses (see Other travel expenses). You can only claim your actual expenses for these vehicles. You must use the logbook method to show your work-related use.

Recent Comments