If you use your own car for work purposes, you can claim a deduction using the cents per kilometre method or logbook method. If you use someone else’s car for work purposes, you can only claim for direct costs you pay for – such as fuel.

You can claim your vehicle expenses if:

✅ You use your car in the course of performing.

✅ Your work duties you attend work-related conferences or meetings away from your normal workplace.

✅ You travel directly between two separate places of employment and one of the places is not your home.

✅ You travel from your normal workplace to an alternative workplace and back to your normal workplace.

✅ You travel from your home to an alternative workplace and then to your normal workplace.

✅ You perform itinerant work.

You can’t claim your vehicle expenses if:

❌ You can’t claim a deduction for normal daily journeys between home and work except in limited circumstances where you carry bulky tools or equipment (such as an extension ladder or cello) that: 1. your employer requires you to use for work 2. you cannot leave at work

❌ If travel is partly private, you can only claim the work-related portion.

❌ You can’t claim a deduction for car expenses that have been salary sacrificed.

❌ You can’t claim a deduction if you have been reimbursed for it.

YOU CAN CALCULATE YOUR CAR EXPENSES IN TWO WAYS: CENTS PER KILOMETRE METHOD AND LOGBOOK METHOD

CENTS PER KILOMETRE METHOD

🔘 You can claim a maximum of 5,000 business kilometres per car, using this method.

🔘 Your claim is based on 68 cents per kilometre.

🔘 You don’t need written evidence but you need to be able to show how you worked out your business kilometres (for example, by producing diary records of work-related trips).

LOGBOOK METHOD

🔘Your claim is based on the businessuse percentage of expenses for the car.

🔘 Expenses include running costs and decline in value. You can’t claim capital costs, such as the purchase price of your car, the principal on any money borrowed to buy it and any improvement costs (eg, adding paint protection and tinted windows).

🔘To work out your business-use percentage, you need a logbook and the odometer readings for the logbook period. The logbook period is a minimum continuous period of 12 weeks.

🔘 You can claim fuel and oil costs based on your actual receipts or you can estimate the expenses based on odometer records that show readings from the start and the end of the period you used the car during the year.

🔘 You need written evidence for all other expenses for the car.

Your vehicle is not considered a car if it is a motorcycle or a vehicle with a carrying capacity of:

❌ one tonne or more, such as a utility truck or panel van

❌ nine passengers or more, such as a minivan.

Keep receipts for your actual expenses. You cannot use the cents per kilometre method for these vehicles. While it is not a requirement to keep a logbook, it is the easiest way to show how you have calculated your work-related use of the vehicle.

KEEPING A LOGBOOK

Your logbook must cover at least 12 continuous weeks. If you started using your car for work-related purposes less than 12 weeks before the end of the year, you can extend the 12-week period into the next financial year.

If you are using the logbook method for two or more cars, keep a logbook for each car and make sure they cover the same period.

Your 12 week logbook is valid for 5 years. However, if your circumstances change (eg, you change jobs) and the logbook is no longer representative, you will need to complete a new 12 week logbook.

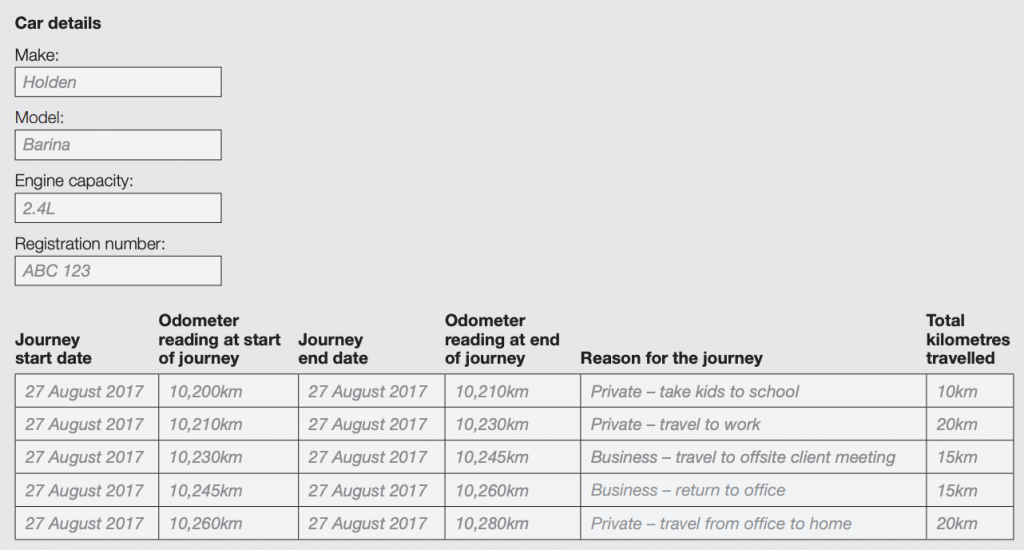

Your logbook can be electronic or paper. The example below has the details you need to keep.

CALCULATE YOUR WORK-RELATED CAR USE

Complete this section after 12 continuous weeks of logbook use

Logbook period (dd/mm/yy to dd/mm/yy)

1️⃣ Calculate the total number of kilometres travelled during the logbook period: x,xxx km

2️⃣ Calculate the number of kilometres you travelled in the course of earning your income during the logbook period: x,xxx km

3️⃣ Calculate the work-related use by dividing the amount at (b) by the amount at (a). Multiply this figure by 100.

YOUR BUSINESS USE PERCENTAGE IS: XX%

Once you’ve calculated your business use percentage, multiply it by your car expenses to figure out your claim.

Car expenses can include running costs such as fuel, oil, and servicing, registration, insurance and vehicle depreciation. You can claim fuel and oil costs based on receipts or you can estimate the expenses based on odometer records that show readings from the start and end of the period you used the car during the year.

You need written evidence for all other expenses for the car.