The ATO allows you to claim vehicle and travel expenses only in certain cases, even your normal trips between home and work. Check here all the cases you can claim vehicle and travel expenses and if you are eligible or not.

The first thing to have in mind is to keep a record of all your travel expenses, including car, fuel and parking. Learn here how to calculate your car expenses.

TRAVELS BETWEEN HOME AND WORK

Trips between home and work are generally considered private travel. In some circumstances, you can claim a deduction for travel between home and work, as well as for some travel between two workplaces.

If your travel was partly private, you can only claim what you incurred in the course of performing your work duties.

You can claim the cost of travelling:

✅ Directly between two separate workplaces – for example, when you have a second job (if one of these places isn’t your home).

✅ From your normal workplace to an alternative workplace that is not a regular workplace (for example, a client’s premises) while still on duty, and back to your normal workplace or directly home.

✅ If your home was a base of employment – you’re required to start your work at home then travel to a workplace to continue your work for the same employer.

✅ If you had shifting places of employment – you regularly work at more than one site each day before returning home.

✅ From your home to an alternative workplace that is not a regular workplace for work purposes, and then to your normal workplace or directly home. This doesn’t apply where the alternative workplace has become a regular workplace.

✅ If you need to carry bulky tools or equipment that your employer requires you to use for work which you can’t leave at your workplace – for example, an extension ladder or a cello.

You can’t claim the cost of driving your car between work and home just because:

❌ You do minor work-related tasks – for example, picking up the mail on the way to work or home.

❌ You have to drive between your home and your workplace more than once a day.

❌ You are on call – for example, you are on stand-by duty and your employer contacts you at home to come into work.

❌ There is no public transport near where you work.

❌ You work outside normal business hours – for example, shift work or overtime.

❌ Your home was a place where you ran your own business and you travelled directly to a place of work where you worked for somebody else.

❌ You do some work at home.

VEHICLE EXPENSES

If you use your own vehicle in performing your work-related duties (including a car you lease or hire), you may be able to claim a deduction for car expenses.

If the travel was partly private, you can claim only the work-related portion.

This information relates to car expenses only. A car is defined as a motor vehicle (excluding motor cycles and similar vehicles) designed to carry a load less than one tonne and fewer than nine passengers. Many four-wheel drive vehicles are included in this definition.

If you use someone else’s car for work purposes, you may be able to claim the direct costs (such as fuel) as a travel expense (see Other travel expenses).

For other vehicles (that are not cars), see Other travel expenses. Other vehicles include:

Motorcycles

Vehicles with a carrying capacity of:

One tonne or more (such as a utility truck or panel van)

Nine passengers or more (such as a minivan).

When working out your claim, you need to use the actual costs of your motor vehicle expenses. You need to keep receipts for the actual costs you incur such as petrol and oil. You can use a logbook or diary to separate private use from work-related trips.

You can claim a deduction for work-related car expenses if you use your own car in the course of performing your job as an employee – for example, to:

✅ Carry bulky tools or equipment (such as an extension ladder or cello) that your employer requires you to use for work and there is no secure storage available at work.

✅ Attend work-related conferences or meetings away from your normal workplace.

✅ Deliver items or collect supplies.

✅ Travel between two separate places of employment, but not if one of the places is your home (for example, when you have a second job).

✅ Travel from your normal workplace to an alternative workplace (that isn’t a regular workplace) back to your normal workplace or directly home.

✅ Travel from your normal workplace or your home to an alternative workplace that is not a regular workplace – for example, a client’s premises

✅ Perform itinerant work.

If you receive an allowance from your employer for car expenses, it is assessable income and the allowance must be included on your tax return. The amount of the allowance is usually shown on your payment summary or income statement.

You can’t claim a deduction for car expenses that have been salary sacrificed or where you have been reimbursed for these expenses.

❌ For motorcycles and other vehicles (that are not cars), you can’t claim work-related deductions under car expenses. However, you may be able to claim for work-related deductions under travel expenses (see Other travel expenses). You can only claim your actual expenses for these vehicles. You must use the logbook method to show your work-related use.

If you use your own car for work purposes, you can claim a deduction using the cents per kilometre method or logbook method. If you use someone else’s car for work purposes, you can only claim for direct costs you pay for – such as fuel.

You can claim your vehicle expenses if:

✅ You use your car in the course of performing.

✅ Your work duties you attend work-related conferences or meetings away from your normal workplace.

✅ You travel directly between two separate places of employment and one of the places is not your home.

✅ You travel from your normal workplace to an alternative workplace and back to your normal workplace.

✅ You travel from your home to an alternative workplace and then to your normal workplace.

✅ You perform itinerant work.

You can’t claim your vehicle expenses if:

❌ You can’t claim a deduction for normal daily journeys between home and work except in limited circumstances where you carry bulky tools or equipment (such as an extension ladder or cello) that: 1. your employer requires you to use for work 2. you cannot leave at work

❌ If travel is partly private, you can only claim the work-related portion.

❌ You can’t claim a deduction for car expenses that have been salary sacrificed.

❌ You can’t claim a deduction if you have been reimbursed for it.

YOU CAN CALCULATE YOUR CAR EXPENSES IN TWO WAYS: CENTS PER KILOMETRE METHOD AND LOGBOOK METHOD

CENTS PER KILOMETRE METHOD

🔘 You can claim a maximum of 5,000 business kilometres per car, using this method.

🔘 Your claim is based on 68 cents per kilometre.

🔘 You don’t need written evidence but you need to be able to show how you worked out your business kilometres (for example, by producing diary records of work-related trips).

LOGBOOK METHOD

🔘Your claim is based on the businessuse percentage of expenses for the car.

🔘 Expenses include running costs and decline in value. You can’t claim capital costs, such as the purchase price of your car, the principal on any money borrowed to buy it and any improvement costs (eg, adding paint protection and tinted windows).

🔘To work out your business-use percentage, you need a logbook and the odometer readings for the logbook period. The logbook period is a minimum continuous period of 12 weeks.

🔘 You can claim fuel and oil costs based on your actual receipts or you can estimate the expenses based on odometer records that show readings from the start and the end of the period you used the car during the year.

🔘 You need written evidence for all other expenses for the car.

Your vehicle is not considered a car if it is a motorcycle or a vehicle with a carrying capacity of:

❌ one tonne or more, such as a utility truck or panel van

❌ nine passengers or more, such as a minivan.

Keep receipts for your actual expenses. You cannot use the cents per kilometre method for these vehicles. While it is not a requirement to keep a logbook, it is the easiest way to show how you have calculated your work-related use of the vehicle.

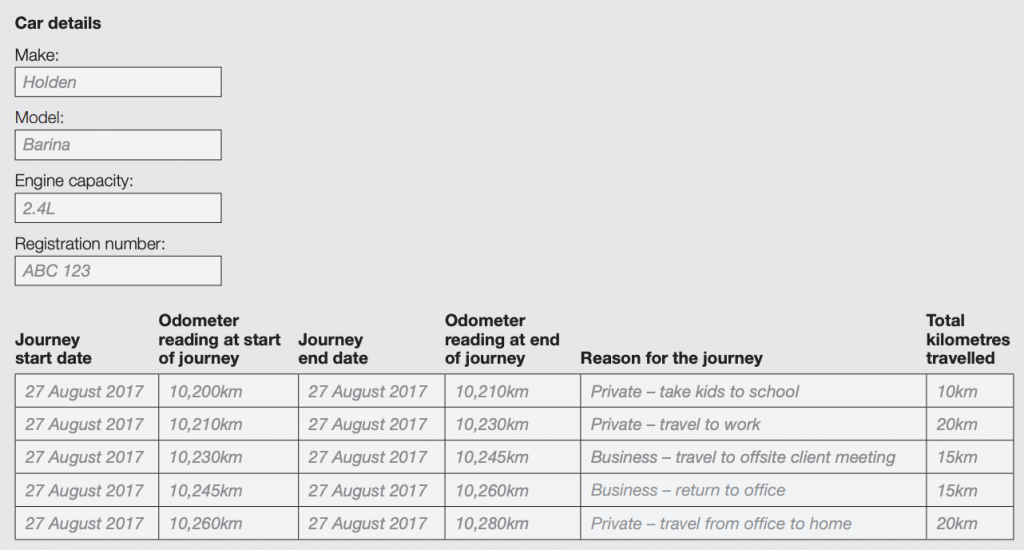

KEEPING A LOGBOOK

Your logbook must cover at least 12 continuous weeks. If you started using your car for work-related purposes less than 12 weeks before the end of the year, you can extend the 12-week period into the next financial year.

If you are using the logbook method for two or more cars, keep a logbook for each car and make sure they cover the same period.

Your 12 week logbook is valid for 5 years. However, if your circumstances change (eg, you change jobs) and the logbook is no longer representative, you will need to complete a new 12 week logbook.

Your logbook can be electronic or paper. The example below has the details you need to keep.

CALCULATE YOUR WORK-RELATED CAR USE

Complete this section after 12 continuous weeks of logbook use

Logbook period (dd/mm/yy to dd/mm/yy)

1️⃣ Calculate the total number of kilometres travelled during the logbook period: x,xxx km

2️⃣ Calculate the number of kilometres you travelled in the course of earning your income during the logbook period: x,xxx km

3️⃣ Calculate the work-related use by dividing the amount at (b) by the amount at (a). Multiply this figure by 100.

YOUR BUSINESS USE PERCENTAGE IS: XX%

Once you’ve calculated your business use percentage, multiply it by your car expenses to figure out your claim.

Car expenses can include running costs such as fuel, oil, and servicing, registration, insurance and vehicle depreciation. You can claim fuel and oil costs based on receipts or you can estimate the expenses based on odometer records that show readings from the start and end of the period you used the car during the year.

You need written evidence for all other expenses for the car.

If you’re enrolled to study in Australia in a course that lasts for six months or more, you may be regarded as an Australian resident for tax purposes. This means:

You pay tax on your earnings at the same rate as other residents

You’re entitled to the benefits of the Australian tax system, such as:

the tax-free threshold (or part of it, if you’re here for only part of the financial year)

tax offsets

generally lower tax rates than a foreign resident.

As an overseas student you probably have a temporary visa, which means that you may be a temporary resident.

LODGING YOUR TAX RETURN

If you worked in Australia, you will probably need to lodge an Australian tax return after 30 June. You can lodge your tax return from your home country.

If you are leaving Australia permanently, you may be eligible to lodge an Australian tax return early. In this case, you must lodge a paper return, which takes longer to process.

If you’re leaving Australia before the end of the income year (30 June), you may be able to lodge your tax return early.

The Australian Taxes Office only accepts early lodgement of tax returns for individuals before the end of the income year if you are an international student and you:

are leaving Australia permanently

will no longer derive Australian-sourced income (other than interest, dividend and royalty income).

Lodge your tax return during the normal lodgement period (1 July to 31 October) if you:

are not leaving Australia permanently

will receive Australian-sourced income (other than interest, dividends and royalties) after leaving Australia

have a Higher Education Loan Program (HELP) or Trade Support Loan (TSL) debt.

CLAIMING YOUR SUPER

Any super contributions paid by your employer must remain in your super fund account while you are in Australia.

You can claim your super if you:

were in Australia on an eligible temporary resident visa (but not if you were on visa subclasses 405 and 410)

had super contributions paid by an employer while you were in Australia.

have left Australia and your working visa has either expired or been cancelled.

When you meet the above conditions, you can then receive your super entitlements as a departing Australia superannuation payment (DASP).

A DASP is not taxed as a superannuation lump sum benefit but is subject to tax under a final withholding tax arrangement.

Your super fund will deduct this tax. Additionally, a DASP is neither your assessable income nor exempt income.

DEPARTING AUSTRALIA SUPERANNUATION PAYMENT (DASP)

If you have worked and earned super while visiting Australia on a temporary visa, you can apply to have this super paid to you as a departing Australia superannuation payment (DASP) after you leave.

Before submitting your DASP application, check with your employer that they have paid all the super they are required to.

If it has been six months or more since you left Australia, your visa has ceased to be in effect and you have not claimed DASP, your super fund will transfer your super money to the ATO as unclaimed super money.

You may be required to provide certified documents for your DASP claim. It’s much easier to have documents certified in Australia so we recommend you do this before you leave. Check with your super fund to confirm what documentation is required.

AUTHORISING SOMEONE TO CLAIM ON YOUR BEHALF

You can authorise someone else to claim DASP for you. The person you authorise will be able to act on your behalf and update your information, so consider carefully who you allow to represent you.

Your representative will need a written authority from you before they can submit your DASP claim.

You can nominate:

a tax agent with full registration or conditional tax agent registration with the Tax Practitioner Board for the purpose of claiming DASP.

a representative if you use a DASP paper form.

Anyone claiming on your behalf using a paper claim form will have to satisfy the holder of your super that they have the authority to make the claim for you. You should check with the holder to find out what documentation they require.

ELIGIBILITY FOR DASP

Generally, you can claim a DASP if the following apply:

You accumulated superannuation while working in Australia on a temporary resident visa issued under the Migration Act 1958 (excluding Subclasses 405 and 410)

Your visa has ceased to be in effect (for example, it has expired or been cancelled)

You have left Australia

You are not an Australian or New Zealand citizen, or a permanent resident of Australia.

CLAIMING GST AND WET REFUNDS

You may be able to claim a refund of the goods and services tax (GST) and wine equalisation tax (WET) included in the price of goods you bought in Australia. You do this at the airport or seaport when you actually leave.

Self-education expenses are the costs you incur to undertake a course of study at a school, college, university or other recognised place of education.

If you work and study and incur self-education expenses you may be eligible for tax deductions.

ELIGIBILITY TO CLAIM

Your current employment and the course you undertake must have sufficient connection for your self-education expenses to qualify as a work-related tax deduction. If a course of study is too general in terms of your current income-earning activities, the necessary connection between the self-education expense and your income-earning activity does not exist.

A tax deduction for your self-education expenses related to your work as an employee is available if you work and study at the same time and can satisfy any of these conditions:

✅ You are upgrading your qualifications for your current employment – for example, upgrading from a Bachelor qualification to a Masters qualification

✅ You are improving specific skills or knowledge used in your current employment – for example, a course that will allow you to operate more machinery at work

✅ You are employed as a trainee and you are undertaking a course that forms part of that traineeship – for example, an overseas trained person employed as an intern while doing a bridging course

✅ You can show that at the time you were working and studying, your course led, or was likely to lead to an increase in employment income – for example, a teacher who will automatically get a pay increase as a result of completing the course.

ELIGIBLE COURSES

Self-education expenses are deductible when the course you undertake leads to a formal qualification and meets the following conditions.

The course must have a sufficient connection to your current work activities as an employee and:

✅ Maintain or improve the specific skills or knowledge you require in your current work activities

✅ Result in, or is likely to result in, an increase in your income from your current work activities.

You can’t claim a deduction for self-education expenses for a course that doesn’t have a sufficient connection to your current work activities even though it:

❌ Might be generally related to it

❌ Enables you to get new employment – such as moving employment as a nurse to employment as a doctor.

EXPENSES YOU CAN CLAIM

You can claim a deduction for following expenses related to your eligible self-education:

✅ Accommodation and meals (if away from home overnight)

✅ Car expenses

✅ Computer consumables

✅ Course fees

✅ Decline in value for depreciating assets (cost exceeds $300)

✅ Purchase of equipment or technical instruments (costing $300 or less)

✅ Equipment repairs

✅ Fares

✅ Home office running costs

✅ Interest

✅ Internet usage (excluding connection fees)

✅ Parking fees (only for work-related claims)

✅ Phone calls

✅ Postage

✅ Stationery

✅ Student union fees

✅ Student services and amenities fees

✅ Textbooks

✅ Trade, professional, or academic journals

✅ Travel to-and-from place of education (only for work-related claims).

Some travel for journeys can’t be claimed, but you may be able to offset the cost of these journeys against the $250 reduction.

If an expense is partly for your self-education and partly for other purposes, you can only claim the amount that relates to your self-education as a deduction.

EXPENSES YOU CAN’T CLAIM

You can’t claim the following expenses in relation to your self-education:

❌ Tuition fees paid by someone else

❌ Repayments of Higher Education Loan Program (HELP) loans (although the fees paid by some HELP loans are)

Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

When you start a business, there are tax and super responsibilities you need to be aware of, including:

The tax implications of your business structure

Whether you’re entitled to an ABN

Registering your business

Records you need to keep

Deductions you can claim.

As you get your business up and running, there are a few things you may need to consider, including:

When your tax and other obligations start – this will depend on whether you are in business yet

The implications of the structure you choose – tax and legal

The location of your business (such as working from home).

BUSINESS STRUCTURE

There are four commonly used business structures in Australia:

🔘 Sole trader

🔘 Partnership

🔘 Company

🔘 Trust

It’s important to understand the responsibilities of each structure because the structure you choose may affect:

🔘 The tax you’re liable to pay 🔘 Asset protection 🔘 Costs.

You’re not locked into any structure and you can change the structure as your business changes or grows.

If you’re unsure which structure to choose, we recommend you contact us.

As soon as your business is running you’re going to face new obligations. Understanding what you need to do from an early stage will help you stay on top of things.

REGISTER YOUR BUSINESS

When you start your business there are a number of registrations you need to consider.

GET AN ABN

If you’re starting a new business you may need an Australian business number (ABN). An ABN is a unique 11-digit identifier that makes it easier for businesses and all levels of government to interact. Not everyone is entitled to an ABN, so the registration process will ask specific questions to determine your entitlement to an ABN.

Not everyone is entitled to an ABN. You’re entitled to an ABN if you’re:

✔️ Carrying on or starting an enterprise in Australia

✔️ Making supplies connected with Australia’s indirect tax zone

✔️A Corporations Act company.

To work as a business you’ll need an ABN, which generally means you:

🔘 Provide products and services directly to your customers, whether that’s the public or other businesses

🔘 Source your own customers, for example by advertising your products and services

🔘 Quote and invoice for work, including setting or negotiating prices

🔘 Have a separate business bank account and your own business insurance such as public liability and WorkCover

🔘 Lodge and report all business income, even if the business earnings are below the tax free threshold.

You will need an ABN to:

✔️ Operate in the GST system, including claiming GST credits

✔️ Avoid pay as you go (PAYG) tax on payments you receive

✔️ Confirm your business identity to others when ordering and invoicing

✔️ Connect to Manage ABN Connections or get an AUSkey to transact online with government agencies

✔️ Be endorsed as a gift deductible recipient or an income tax exempt charity.

REGISTER YOUR BUSINESS NAME

If you’re applying for an Australian business number (ABN), you can also apply for a business name and register for secure online authentication and taxes, like GST and PAYG withholding, at the same time.

Most businesses will need to apply for a registered business name with the Australian Securities & Investments Commission (ASIC).

You can carry on a business in your own name without registering a business name if you don’t change or add anything to your name. For example, John Smith doesn’t have to register a name to trade as J Smith or John Smith, but he does to trade as John Smith Landscaping.

To apply for a registered business name you will need to have applied for or have an ABN.

All businesses will need to register all trading names as a business name with ASIC in order to continue operating with it. ABN Lookup will only display business names registered with ASIC from this date.

GETTING AN AUSTRALIAN COMPANY NUMBER

If you plan to run your business through a company, you need to register your company and get an ACN. You do this with ASIC when you start your company. You need to get your ACN before you can get your ABN and tax registrations

RECORD KEEPING

You need to set up a good record keeping system to track your income and expenses right from the start. This helps you know how your business is going, as well as meet your tax responsibilities and be able to claim all the deductions to which you are entitled.

HIRING WORKERS

If you’re thinking of taking on workers it’s important to understand you will have extra responsibilities. For example, you may have to:

Deduct tax from their pay and send it to the ATO Pay super contributions to their nominated super fund, and Pay fringe benefits tax if you provide them with benefits in addition to their wages.

PAYING TAX IN YOUR FIRST YEAR

In your first year of business, you can stay on top of your obligations by:

Making tax pre-payments into your tax bill account

Putting money aside for your expected tax bill

Voluntarily entering into instalments

PAYING TAX BY INSTALMENTS

Once you lodge your first income tax return and report a tax-payable amount above a certain threshold, you will automatically enter the pay-as-you-go (PAYG) instalment system.

If you voluntarily enter into instalments prior to lodgement of your first tax return, you will be able to make quarterly payments towards you tax bill.

REPORTING

Once you’re up and running, you’ll need to report your business income and other tax information. The key reports you should be aware of are:

Business Activity Statement (BAS)

🔘 The main taxes you will report on will be GST (if you’re registered for GST) 🔘Any tax you withhold from employees’ pay 🔘 Instalments towards your own tax once you are in the pay as you go instalments system. 🔘Income tax return

To report your personal and business income and claim deductions.

Recent Comments